Listen to the second segment of the October 30, 2006, Closer Look show from the nationwide K-Love radio station. The interviewer asks questions of representatives of both political parties. Most of the interviewees are conservative (2 Republicans and 1 conservative Democrat), but this probably reflects the ratio of Christians nationwide. Religion is a natural conservative force in society. But they did at least interview one moderate-liberal among the group.

I think in the coming years more Christians will start to listen to the interests of the Christian Left. It is unquestionably part of the great tradition of Christian thought throughout the centuries to push for more justice for the weakest members of society.

http://www.youtube.com/watch?v=gLhHzbnHAOM

I have posted both what is supposed to be an embedded video and a link to the same on YouTube just in case. It is a video of a local minister here in Oklahoma City named Dr. Robin Meyers, who is the pastor of Mayflower Congregational Church, which is a Universal Church of Christ (UCC) congregation. The UCC is known for its controversial advertisements which were censored by the major networks. Dr. Meyers also writes a regular column for the Oklahoma Gazette, a weekly newspaper that gives a lot of information about local arts and politics. I don't agree with everything Rev. Meyers says (I am not a pantheist -- that is to say, I don't think there are many paths to God), but the points about a country's movement toward fascism are worth listening to.

Tuesday, October 31, 2006

An OMG Poll Result from Cook Political Report

Likely voters on Generic Congressional Ballot (October 26-29, 2006) polling of likely voters:

Democrats: 61%

Republicans: 35%

That is a 26% difference.

Even with gerrymandering, this cannot be good for the Republicans. And to pour salt on an open wound, the gap is getting larger every time they poll.

Democrats: 61%

Republicans: 35%

That is a 26% difference.

Even with gerrymandering, this cannot be good for the Republicans. And to pour salt on an open wound, the gap is getting larger every time they poll.

Monday, October 30, 2006

Watch Out for the Fraud Hobgoblins this Halloween

In line with my previous post, here are some tips on how to avoid fraud. The link above goes to some of the more common frauds committed against unsuspecting consumers. These are the kinds of stories that make ideologies like Libertarianism and "free market Capitalism" so preposterous. And there are many forms of fraud and dishonesty that, in the law, do not rise to the level of criminal behavior. The only way to control such abuses is through a strong legal system that can enforce justice against such prevaricators. It is also why we need punitive damages to be available. We need to make sure that those who intentionally rip people off do not profit from their deception.

One of the hardest to detect is "affinity fraud." I have seen a lot of these in my lifetime that spread in the churches. My people are destroyed for lack of knowledge (Hosea 4:6).

We have bought from the brokers who have broken their oaths

And we're out on the streets with a lump in our throats

The kind of people who commit these kind of white collar crimes are usually very smart and they have become practiced liars. It takes a discerning mind to catch them and warn others of the traps they seek to spring on the gullible.

One of the hardest to detect is "affinity fraud." I have seen a lot of these in my lifetime that spread in the churches. My people are destroyed for lack of knowledge (Hosea 4:6).

We have bought from the brokers who have broken their oaths

And we're out on the streets with a lump in our throats

The kind of people who commit these kind of white collar crimes are usually very smart and they have become practiced liars. It takes a discerning mind to catch them and warn others of the traps they seek to spring on the gullible.

Shocking story about "Liar Loans" in San Francisco

Did I hear that right? 85%(!) of all loans in that area?

The realtors were pushing it because they made $10,000 on every sale. And the poor debtors are ultimately the ones who are going to pay the price, because falsely stating one's income on a mortgage application is a crime.

The parties involved are going to have to be sorted out between those who intentionally lied on their loans and those that were duped.

The realtors were pushing it because they made $10,000 on every sale. And the poor debtors are ultimately the ones who are going to pay the price, because falsely stating one's income on a mortgage application is a crime.

The parties involved are going to have to be sorted out between those who intentionally lied on their loans and those that were duped.

Oklahoma Cities listed in Most Safe and Dangerous

Broken Arrow is a suburb of Tulsa. Norman is a suburb of Oklahoma City. Lawton is in the southwest part of Oklahoma.

Sunday, October 29, 2006

New look and features

I have created a new look and features for my blog. I hope everyone likes it. There is a new keyword function that I have added to the sidebar. The search box is now in the upper left hand part of the page next to the blogger symbol.

Personal Bankruptcies Down 80%

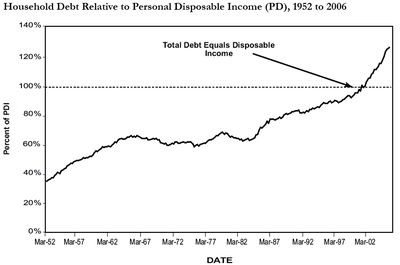

It appears that the debt-to-income ratio keeps going up. Bankruptcies may be down for now, and the President and Congress may have made personal bankruptcy much more difficult and expensive, but the numbers don't lie. Eventually, something will have to give. Unfortunately, things will probably get worse before they get better.

(thanks to The Big Picture Blog for the chart)

Gimme Mine

On another blog recently, a conservative writer argued against the notion of providing health care for all Americans. His argument was that to do so would require him to have to pay for not only his health care, but his neighbors as well. He took moral umbrage at this idea.

This reminded me of another song by Mark Heard, Gimme Mine:

Ever since I was a young boy

I wondered what to be

Watching all the grownups shaking on the money tree

You know that everybody's got their places

Everyone fits just fine: all except me, Lord

Now when You gonna gimme mine?

All across the nation (everywhere) people do their things (pulling their hair)

Pushing on buttons and pulling on different strings

You know that everybody's got their places

Everyone fits just fine: all except me, Lord

Now when You gonna gimme mine?

Now when You gonna gimme importance?

When You gonna gimme wealth?

When You gonna make me like everybody else?

I got to get me a high position, got to get me a Cadillac

Got to get me a raise, I got to get me a heart attack

You know that everybody's got their places

Everyone fits just fine all except me, Lord

Now when You gonna gimme mine?

Oooh working at the Neiman Marcus, working at the five and dime

Got to have the money gonna make it in the nick of time

You know that everybody's got their places

Everyone fits just fine all except me, Lord

Now when You gonna gimme mine?

From Eye of the Storm and Fingerprint. With thanks to the Mark Heard Lyric Project

______________________________

Notice how this song is contrary to the "Gospel of Wealth" that is getting preached to so many Christians today. It is all about the notion that financial success is tied to piety. It says that people are not poor due to some moral failure.

But it was Jesus himself that told the rich young ruler to give away all his wealth. The Gospel of Wealth is a Capitalist construct, not a Christian one. It is pretty unique to our culture. Hoarding of resources is more of a greedy concept than a Christian one; so why are so many Christian leaders pushing it as moral?

This reminded me of another song by Mark Heard, Gimme Mine:

GIMME MINE

by Mark Heard

by Mark Heard

Ever since I was a young boy

I wondered what to be

Watching all the grownups shaking on the money tree

You know that everybody's got their places

Everyone fits just fine: all except me, Lord

Now when You gonna gimme mine?

All across the nation (everywhere) people do their things (pulling their hair)

Pushing on buttons and pulling on different strings

You know that everybody's got their places

Everyone fits just fine: all except me, Lord

Now when You gonna gimme mine?

Now when You gonna gimme importance?

When You gonna gimme wealth?

When You gonna make me like everybody else?

I got to get me a high position, got to get me a Cadillac

Got to get me a raise, I got to get me a heart attack

You know that everybody's got their places

Everyone fits just fine all except me, Lord

Now when You gonna gimme mine?

Oooh working at the Neiman Marcus, working at the five and dime

Got to have the money gonna make it in the nick of time

You know that everybody's got their places

Everyone fits just fine all except me, Lord

Now when You gonna gimme mine?

From Eye of the Storm and Fingerprint. With thanks to the Mark Heard Lyric Project

______________________________

Notice how this song is contrary to the "Gospel of Wealth" that is getting preached to so many Christians today. It is all about the notion that financial success is tied to piety. It says that people are not poor due to some moral failure.

But it was Jesus himself that told the rich young ruler to give away all his wealth. The Gospel of Wealth is a Capitalist construct, not a Christian one. It is pretty unique to our culture. Hoarding of resources is more of a greedy concept than a Christian one; so why are so many Christian leaders pushing it as moral?

Saturday, October 28, 2006

A pretty scary report

From the article:

"We all agree on what the choices are and what the numbers are," Fraser says.

Their basic message is this: If the United States government conducts business as usual over the next few decades, a national debt that is already $8.5 trillion could reach $46 trillion or more, adjusted for inflation. That's almost as much as the total net worth of every person in America — Bill Gates, Warren Buffett and those Google guys included.

A hole that big could paralyze the U.S. economy; according to some projections, just the interest payments on a debt that big would be as much as all the taxes the government collects today.

And every year that nothing is done about it, Walker says, the problem grows by $2 trillion to $3 trillion.

"We all agree on what the choices are and what the numbers are," Fraser says.

Their basic message is this: If the United States government conducts business as usual over the next few decades, a national debt that is already $8.5 trillion could reach $46 trillion or more, adjusted for inflation. That's almost as much as the total net worth of every person in America — Bill Gates, Warren Buffett and those Google guys included.

A hole that big could paralyze the U.S. economy; according to some projections, just the interest payments on a debt that big would be as much as all the taxes the government collects today.

And every year that nothing is done about it, Walker says, the problem grows by $2 trillion to $3 trillion.

Pessimism at Dow 12,000

From the article:

Tice worries about credit growth at all levels. The U.S.’s $70 billion current account deficit, he argues, suggests the country can’t afford its standard of living without borrowing from abroad. “I believe that the credit expansion will end in tears,” he says.

In particular, Tice warns about real estate debt. He points to sagging property values in San Diego, Las Vegas and Miami. Stripped of their ability to flip, homeowners in those markets are thus likely to get stuck paying off mortgages based on inflated home prices.

___________________________

Tice's view is considered the "contrarian" view to the idea that we are entering another bull market. An example of the opposite view is at an NPR story here.

The problem with the NPR report is that it doesn't tell the whole story. (Imagine that, a news report that doesn't tell the whole story!) Because of the falling home prices, there are many people who will not be able to refinance due to the fact that they no longer qualify because of a lack of equity -- or even negative equity.

Then there will be those who will want to sell in order to relocate for employment purposes, who won't be able to sell without a substantial loss.

Then there will be those who will be able to refinance, but who will have to pay the prepayment penalty -- some of whom will probably have to take money out of savings or retirement to finance the refinance.

These situations will have repurcussions several years down the road. Americans are not saving enough. What are they going to rely on when they reach retirement age? Social Security will not be enough. Many companies are getting sold and the retirement funds raided. Other companies are bankrupting their obligations for pensions and health care. How are the injured workers who were counting on their pensions going to made whole? (Hint: don't count on the Pension Benefit Guaranty Corporation (PBGC). Here is a news article that points out part of the problem. From the article:

The pension problem has caused PBGC itself to be underfunded. After assuming the UAL plans, it will owe about $62.3 billion in promised benefits to more than 1.1 million people, including more than 500,000 current retirees, but its assets are only $39 billion.

It is possible we won't see a severe impact immediately, but what are we going to do when the baby boomers start to retire and don't have enough retirement savings?

Tice worries about credit growth at all levels. The U.S.’s $70 billion current account deficit, he argues, suggests the country can’t afford its standard of living without borrowing from abroad. “I believe that the credit expansion will end in tears,” he says.

In particular, Tice warns about real estate debt. He points to sagging property values in San Diego, Las Vegas and Miami. Stripped of their ability to flip, homeowners in those markets are thus likely to get stuck paying off mortgages based on inflated home prices.

___________________________

Tice's view is considered the "contrarian" view to the idea that we are entering another bull market. An example of the opposite view is at an NPR story here.

The problem with the NPR report is that it doesn't tell the whole story. (Imagine that, a news report that doesn't tell the whole story!) Because of the falling home prices, there are many people who will not be able to refinance due to the fact that they no longer qualify because of a lack of equity -- or even negative equity.

Then there will be those who will want to sell in order to relocate for employment purposes, who won't be able to sell without a substantial loss.

Then there will be those who will be able to refinance, but who will have to pay the prepayment penalty -- some of whom will probably have to take money out of savings or retirement to finance the refinance.

These situations will have repurcussions several years down the road. Americans are not saving enough. What are they going to rely on when they reach retirement age? Social Security will not be enough. Many companies are getting sold and the retirement funds raided. Other companies are bankrupting their obligations for pensions and health care. How are the injured workers who were counting on their pensions going to made whole? (Hint: don't count on the Pension Benefit Guaranty Corporation (PBGC). Here is a news article that points out part of the problem. From the article:

The pension problem has caused PBGC itself to be underfunded. After assuming the UAL plans, it will owe about $62.3 billion in promised benefits to more than 1.1 million people, including more than 500,000 current retirees, but its assets are only $39 billion.

It is possible we won't see a severe impact immediately, but what are we going to do when the baby boomers start to retire and don't have enough retirement savings?

Merry Christmas, You're Fired

From the news article today:

The first group of employees to lose their jobs at Bridgestone/Firestone's Dayton Tire factory in Oklahoma City will learn details of their severance packages at meetings today and Friday, the company said.

...

But company spokesman Dan MacDonald said the factory closure comes after the [union] contract has expired, so the job losses are terminations.

"You can't call it a layoff, since those employees will not be called back to the plant," MacDonald said.

...

The company gave its official notice in July, saying the factory would close by Dec. 31 with the loss of more than 1,400 jobs. The typical production worker at Dayton makes about $900 a week, not including benefits, according to the company.

Local union officials said the company has put employees in Oklahoma City in a tough position, especially as the remainder of the job losses — 1,000 — will come in the week before Christmas.

The first group of employees to lose their jobs at Bridgestone/Firestone's Dayton Tire factory in Oklahoma City will learn details of their severance packages at meetings today and Friday, the company said.

...

But company spokesman Dan MacDonald said the factory closure comes after the [union] contract has expired, so the job losses are terminations.

"You can't call it a layoff, since those employees will not be called back to the plant," MacDonald said.

...

The company gave its official notice in July, saying the factory would close by Dec. 31 with the loss of more than 1,400 jobs. The typical production worker at Dayton makes about $900 a week, not including benefits, according to the company.

Local union officials said the company has put employees in Oklahoma City in a tough position, especially as the remainder of the job losses — 1,000 — will come in the week before Christmas.

______________________________

This is just one of the many manufacturing job plant closings in the Oklahoma City area. Given the high wages these workers garnered for the local area, it will be very difficult for them to find work that will be comparable in pay and benefits to the job they are losing.

Friday, October 27, 2006

Top 10 Foreclosure Cities

I am a little surprised by the inclusion of Dallas and Ft. Worth, TX. Neither of these is considered to be a real "bubble market" (and they are not too far from here). I am wondering if it has more to do with people buying homes for themselves when they could not afford it, or if it was due to a high number of borrowers that bought a house using "exotic" loans such as ARMs and I/O.

Thursday, October 26, 2006

Credit Risk for Employers and National Security

A good discussion of credit risk, employment and national security in the Warren Reports section at Talking Points Memo.

Wednesday, October 25, 2006

News from a Foreclosure Attorney

I spoke with an attorney in town today whose firm does a lot of foreclosures in the Oklahoma City area. I asked him if he was seeing an uptick in foreclosures recently. He said there was a small increase in foreclosures, but he expects things to really pick up next year. It is not due as much to the California and Florida bubbles -- although that will contribute some due to the reduction in opportunities for *1031 investments -- but rather due to local market and employment conditions. Both General Motors and the Dayton tire plant (as well as a couple other major employers in the Oklahoma City area) have closed or are closing their doors. As a result, some 5000+ high-wage workers have been or will be laid off and their severance pay is expected to start running out some time next spring.

He told me that he is already also seeing a noticeable increase in the availability of HUD homes that have already been through foreclosure.

He seems to think that I would be wise to wait another year before buying a house in the Oklahoma City area as he expects house prices to drop between 10-20% in the next year.

What that means is that my previous post indicating that OKC home prices seem pretty stable was based on incomplete information.

_____________________________

*Internal Revenue Code Section 1031 is a tool for deferring capital gains tax on commercial/investment transactions. This Section allows taxpayers to exchange real or personal property for new "like-kind" property, while deferring recognition of any capital gains. Section 1031 creates the ability for sellers to defer capital gains on investment property by placing the sale proceeds with a "Qualified Intermediary" for up to 180 days until the closing of the purchase of the replacement property.

You learn something new every day.

He told me that he is already also seeing a noticeable increase in the availability of HUD homes that have already been through foreclosure.

He seems to think that I would be wise to wait another year before buying a house in the Oklahoma City area as he expects house prices to drop between 10-20% in the next year.

What that means is that my previous post indicating that OKC home prices seem pretty stable was based on incomplete information.

_____________________________

*Internal Revenue Code Section 1031 is a tool for deferring capital gains tax on commercial/investment transactions. This Section allows taxpayers to exchange real or personal property for new "like-kind" property, while deferring recognition of any capital gains. Section 1031 creates the ability for sellers to defer capital gains on investment property by placing the sale proceeds with a "Qualified Intermediary" for up to 180 days until the closing of the purchase of the replacement property.

You learn something new every day.

Tuesday, October 24, 2006

The Great Risk Shift

Today on Calculated Risk (see link to his website in the sidebar), CR placed a post about expected rising foreclosures -- which is expected to rise to 4% of mortgaged homes, an unprecedented high.

What I think is not commonly discussed in the coming real estate crash and ensuing mass foreclosures is how many people counted on their home being paid off during their retirement years. Now many more Americans (how ever many it ends up being) will feel disenfranchised again. In the macro sense, this will only add to the sense that, in America, you now cannot make it as a success (financially, anyway) in life unless you already start with capital (born into wealth) or find some way to steal it (as in the accounting industry and law practice "all great wealth starts with a crime"). This is not good for the country.

Now that many ordinary middle class and lower middle class Americans have been sold on the fraudulent idea that housing always goes up in value and everyone can afford a home, the ensuing bust will lead to a sense of despair and depression in the same population. The psychological effect on these people will be much more severe than simply losing money in the stock market, and it will impact more than just those who lose their homes. The idea of losing your home will have, I think, a much more severe and long-lasting impact than the stock market crash did in 2000.

And don't forget the new bankruptcy law that makes it much harder -- and much more expensive -- to file for bankruptcy. That many more people will be priced out of the bankruptcy market and will not be able to have the "fresh start" that bankruptcy is supposed to afford. The threat of bankruptcy was supposed to put the risk on the lender, rather than the consumer, to make only loans that have a high likelyhood of being paid back. Traditionally, real estate loans were among the least risky of all loans. That is why the interest rate was so low. Owning a home was supposed to be a sign of stability.

This is just another example where the "risk of loss" has been shifted from the educated and wealthy to the ignorant and poor. Again, traditionally, we have moved away from the concept of caveat emptor ("let the buyer beware") to one where the seller accepts more of the risk of loss. The reason for this is that the seller, being a merchant in goods of a kind, was in a better position to know the product and the risks that could be suffered by the user or consumer. Therefore, we required the seller to make the product safe for the consumer, and, in the case of products liability, strict liability was imposed on the seller as a means of insuring that products were tested to be safe for the ultimate user or consumer of the product. We now seem to be shifting the risk of loss of debt to the consumer.

Another way that the risk of loss has been shifted away from the lenders is through the use of "tranching." Why bother making safe loans when you can merely sell the loan to someone else? Which leads to another axiom of great wealth creation: always play with OPM -- other people's money. That is exactly what the lenders are doing. They are playing with our money. Therefore the risk of loss has shifted from those who should be taking the risk -- those who best understand the risk and consequences, the seller -- to those who are least able to afford or understand the consequences: the consumer.

More on this later...

What I think is not commonly discussed in the coming real estate crash and ensuing mass foreclosures is how many people counted on their home being paid off during their retirement years. Now many more Americans (how ever many it ends up being) will feel disenfranchised again. In the macro sense, this will only add to the sense that, in America, you now cannot make it as a success (financially, anyway) in life unless you already start with capital (born into wealth) or find some way to steal it (as in the accounting industry and law practice "all great wealth starts with a crime"). This is not good for the country.

Now that many ordinary middle class and lower middle class Americans have been sold on the fraudulent idea that housing always goes up in value and everyone can afford a home, the ensuing bust will lead to a sense of despair and depression in the same population. The psychological effect on these people will be much more severe than simply losing money in the stock market, and it will impact more than just those who lose their homes. The idea of losing your home will have, I think, a much more severe and long-lasting impact than the stock market crash did in 2000.

And don't forget the new bankruptcy law that makes it much harder -- and much more expensive -- to file for bankruptcy. That many more people will be priced out of the bankruptcy market and will not be able to have the "fresh start" that bankruptcy is supposed to afford. The threat of bankruptcy was supposed to put the risk on the lender, rather than the consumer, to make only loans that have a high likelyhood of being paid back. Traditionally, real estate loans were among the least risky of all loans. That is why the interest rate was so low. Owning a home was supposed to be a sign of stability.

This is just another example where the "risk of loss" has been shifted from the educated and wealthy to the ignorant and poor. Again, traditionally, we have moved away from the concept of caveat emptor ("let the buyer beware") to one where the seller accepts more of the risk of loss. The reason for this is that the seller, being a merchant in goods of a kind, was in a better position to know the product and the risks that could be suffered by the user or consumer. Therefore, we required the seller to make the product safe for the consumer, and, in the case of products liability, strict liability was imposed on the seller as a means of insuring that products were tested to be safe for the ultimate user or consumer of the product. We now seem to be shifting the risk of loss of debt to the consumer.

Another way that the risk of loss has been shifted away from the lenders is through the use of "tranching." Why bother making safe loans when you can merely sell the loan to someone else? Which leads to another axiom of great wealth creation: always play with OPM -- other people's money. That is exactly what the lenders are doing. They are playing with our money. Therefore the risk of loss has shifted from those who should be taking the risk -- those who best understand the risk and consequences, the seller -- to those who are least able to afford or understand the consequences: the consumer.

More on this later...

Saturday, October 21, 2006

Monopoly game: Housing Bust Edition

{kind=link}

***See comments for updated link***

Thanks to Aaron Erimez for the "new and improved" image!

Thanks to Aaron Erimez for the "new and improved" image!

The Orphans of God

THE ORPHANS OF GOD

by Mark Heard

by Mark Heard

I will rise from my bed with a question again

As I work to inherit the restless wind

The view from my window is cold and obscene

I want to touch what my eyes have not seen

But they have packaged our virtue in cellulose dreams

And sold us the remnants 'til our pockets are clean

Til our hopes fall 'round our feet

Like the dust and dead leaves

And we end up looking like what we believe

We are soot-covered urchins running wild and unshod

We will always be remembered as the orphans of God

They will dig up these ruins and make flutes of our bones

And blow a hymn to the memory of the orphans of God

Like bees in a bottle we are flying at fate

Beating our wings against the walls of this place

Unaware that the struggle is the blood of the proof

In choosing to believe the unbelievable truth

But they have captured our siblings and rendered them mute

They've disputed our lineage and poisoned our roots

We have bought from the brokers who have broken their oaths

And we're out on the streets with a lump in our throats

We are soot-covered urchins running wild and unshod

We will always be remembered as the orphans of God

They will dig up these ruins And make flutes of our bones

And blow a hymn to the memory of the orphans of God

You can listen to the song here. It is song #4.

You can get his High Noon CD (a compilation of his best songs from his last three CDs) from Amazon.com.

This is an example of the kind of musical poetry that has had such a profound effect on me. Although it probably was never meant to have a political application, I thought of this song when I heard about David Kuo's new book about how the Bush administration secretly laughed at conservative Christians who gave them all of their political support. I have boldened the passages that can be interpreted to apply to the current political situation.

I had my disillusionment with political conservatism just before I entered law school and the Republican party in general in 2002. My disillusionment with Christian fundamentalism happened around 1990 (I entered law school in 1992). That is partially why I did not discover Mark Heard's later works (such as this one) until a few years after law school. And it was only recently that I could find his music on CD.

Mark Heard was one of my favorite artists in my early formative years as a teenager and young adult. Even his early music on Stop the Dominoes, Victims of the Age and the "unplugged" Eye of the Storm still seems way ahead of its time lyrically; although his later albums are definitely more refined both musically and lyrically.

Anyway, back to David Kuo's comments that I saw: many of his complaints are about lack of funding for government programs to assist the poor through the churches. His focus is too narrow. He, like many of the conservative Christian movement, think that any help for the poor must come through the churches so that the help they provide can be used to further their ministry. However, there is nothing that I read in the Gospels or the New Testament that says that helping the less fortunate or disenfranchised must come through the church. I see nothing unchristian about helping the less fortunate in their worldly needs by lobbying our elected officials to fund programs to feed, shelter and clothe the needy and provide them with medical attention when they need it. For that matter, as I have pointed out several times before, I think that everyone should have access to medical care -- because it is the humanitarian thing to do. Medical care, at its core, is based the humanitarian concept of alleviating unnecessary suffering and promoting the welfare of mankind.

There was a time when the Christian movement was one that promoted humanism. Martin Luther and Erasmus during the Renaissance promoted Religious Humanism. An excerpt from Answers.com:

Religious humanism

Religious humanism is the branch of humanism that considers itself religious (based on a functional definition of religion), or embraces some form of theism, deism, or supernaturalism, without necessarily being allied with organized religion, as such. It is often associated with artists, liberal Christians, and scholars in the liberal arts. Other types of people that may be considered religious humanists are those who, despite believing in a religion, don't consider it necessary to derive all their moral values from it. Some feel that, because their religious beliefs are moral, and therefore humane, they are humanists. In particular, it is not uncommon for religious humanitarians to be referred to as humanists, although the accuracy of this usage is disputed.

A number of religious humanists feel that secular humanism is too coldly logical and rejects the full emotional experience that makes us human. From this comes the notion that secular humanism is inadequate in meeting the human need for a socially fulfilling philosophy of life. Disagreements over things of this nature have resulted in friction between secular and religious humanists, despite their commonalities.

I have always used the term "Theistic Humanist" to describe my philosophy. It is similar to Religious Humanism as described above, but I accept the power of reason to solve many -- if not most -- of life's problems.

So, from my perspective, David Kuo is trying to bring Christianity's humanism to an administration that, in reality, believes in an Ayn Randian objectivism. The two are not really compatible ideas. The objectivists are untimately going to see any government spending to help the less fortunate as a movement toward socialism -- which they oppose feverishly. If Mr. Kuo -- or any other Christian -- wants to push for more government funding to alleviate social problems related to poverty, they will need to support a political group or party that is not opposed to government spending to relieve those problems. Pretty much by definition that historically means supporting the Democratic party (at least as it has existed in the last 50+ years).

Thursday, October 19, 2006

Keith Olbermann on the Death of Habeas Corpus

I don't know if the link above will work. If it does not, please let me know.

In the game of chess, there is a saying: "the threat is greater than its execution." As applied to the threat being used to justify eliminating Habeas Corpus (terrorism) is greater than its execution (actually blowing up things). The response (elimination of our civil liberties in response to security concerns) is a result that could not have have been achieved without the threat.

But we should be reminded of a saying attributed to Benjamin Franklin: "Those who would give up Essential Liberty to purchase a little Temporary Safety deserve neither Liberty nor Safety."

For more on the basics of Habeas Corpus see this entry at Answers.com (particularly the entry from the Legal Encyclopedia).

In the game of chess, there is a saying: "the threat is greater than its execution." As applied to the threat being used to justify eliminating Habeas Corpus (terrorism) is greater than its execution (actually blowing up things). The response (elimination of our civil liberties in response to security concerns) is a result that could not have have been achieved without the threat.

But we should be reminded of a saying attributed to Benjamin Franklin: "Those who would give up Essential Liberty to purchase a little Temporary Safety deserve neither Liberty nor Safety."

For more on the basics of Habeas Corpus see this entry at Answers.com (particularly the entry from the Legal Encyclopedia).

Wednesday, October 18, 2006

Oklahoma City Housing

If you are thinking of moving to Oklahoma City because of a job, or just want a cheaper place to live and still have access to "quality of life" amenities such as art, music, sports and the like, I have decided to use this post to help you find the best parts of Oklahoma City (and surrounding area) in which to look for a house. I have lived here my entire life, so I am pretty familiar with the area.

First off, if you want to look at the neighborhood crime statistics in Oklahoma City proper without actually visiting it, you can go to Channel 9's (CBS) CrimeTracker website.

As a general rule, northwest Oklahoma City is a better quadrant than the others, although far southwest OKC is also being developed with nicer neighborhoods. When I was out home-hunting recently, I looked for a home in the zip codes 73120, 73116 and 73120 in that order. If you are fabulously wealthy, the area of OKC you would want to live in to be ostentatious would be Nichols Hills, which is 73116. The Village, which is the middle class area just north of Nichols Hills is 73120. However, the 73120 zip code includes a large part of NW OKC.

Now, if you don't mind commuting up to 30 minutes, communities outside of Oklahoma City proper provides nice, generally safe areas to live. For example:

Norman (where the University of Oklahoma is located) is about 20-40 minutes directly south of OKC, depending on the traffic. The west side of I-35 and far east part have the nicest homes. However, there are very few unsafe areas there. The "worst" areas are the ones around the Griffin Memorial Hospital, where patients with mental illnesses or substance abuse problems are housed (although I think they may have moved it from its original location); and an area very close to Campus Corner that has a reputation for being "slum housing." Norman is the home of the actor James Garner and several country musicians such as Toby Keith, Vince Gill and Conway Twitty.

Edmond (where the University of Central Oklahoma is located) is north of Oklahoma City by almost the same distance as Norman is to the south. Edmond is generally regarded to be a town that is middle class to upper class. Noted dignitaries or celebrities include olympic 5-medal gymnastics winner Shannon Miller, onetime local newscaster cum restaurant entrepreneur Vince Orza (who also ran a couple of times for Governor). Edmond is also home to the Oak Tree Golf Club where several pros make their home. The "worst" areas are the homes near the railroad tracks by the post office. Edmond's claim to infamy was when Patrick Sherrill walked into the Edmond post office and killed several of the other employees and then committed suicide. (I only mention this because I worked there at the same time as Patrick Sherrill. I was a distribution clerk and he was a carrier. I took his mail to him after it had been sorted. It is kind of scary to think that my work station -- the PO Boxes from 400-1200 -- was the area where he killed the most people. I guess in hindsight I should count being let go during my probation just prior to this incident as being a blessing in disguise.)

Piedmont, which is northwest of Oklahoma City is a small community where many parents are moving to for its public schools, which are considered to be among the best in the Oklahoma City area.

Mustang is southwest of Oklahoma City and has the same reputation as Piedmont. The home values in Mustang and Piedmont have risen very fast in the last few years. I guess if there are bubble areas of Oklahoma City, this would be two of them.

Houses in the OKC area will generally range from $45 per square foot for less desirable areas to $80 sf for the nicest areas (like the ones I was looking for). For the most part, most of OKC is very affordable and can be bought by middle income earners for 20% down and 20% of gross income -- which is the general rule for home affordability. A check on the Multi Listing System (MLS) will confirm that it is possible to buy medium-sized home with yard space for kids and pets for a reasonable price.

I suspect Oklahoma City and the surrounding area will get hit by the Housing Bubble we hear so much about in a few years, but I somehow doubt that we will get hit as hard.

While life is slower here, we still have access to things that other big cities have; but you will probably encounter fewer stressed-out, rude people in the process of enjoying them.

First off, if you want to look at the neighborhood crime statistics in Oklahoma City proper without actually visiting it, you can go to Channel 9's (CBS) CrimeTracker website.

As a general rule, northwest Oklahoma City is a better quadrant than the others, although far southwest OKC is also being developed with nicer neighborhoods. When I was out home-hunting recently, I looked for a home in the zip codes 73120, 73116 and 73120 in that order. If you are fabulously wealthy, the area of OKC you would want to live in to be ostentatious would be Nichols Hills, which is 73116. The Village, which is the middle class area just north of Nichols Hills is 73120. However, the 73120 zip code includes a large part of NW OKC.

Now, if you don't mind commuting up to 30 minutes, communities outside of Oklahoma City proper provides nice, generally safe areas to live. For example:

Norman (where the University of Oklahoma is located) is about 20-40 minutes directly south of OKC, depending on the traffic. The west side of I-35 and far east part have the nicest homes. However, there are very few unsafe areas there. The "worst" areas are the ones around the Griffin Memorial Hospital, where patients with mental illnesses or substance abuse problems are housed (although I think they may have moved it from its original location); and an area very close to Campus Corner that has a reputation for being "slum housing." Norman is the home of the actor James Garner and several country musicians such as Toby Keith, Vince Gill and Conway Twitty.

Edmond (where the University of Central Oklahoma is located) is north of Oklahoma City by almost the same distance as Norman is to the south. Edmond is generally regarded to be a town that is middle class to upper class. Noted dignitaries or celebrities include olympic 5-medal gymnastics winner Shannon Miller, onetime local newscaster cum restaurant entrepreneur Vince Orza (who also ran a couple of times for Governor). Edmond is also home to the Oak Tree Golf Club where several pros make their home. The "worst" areas are the homes near the railroad tracks by the post office. Edmond's claim to infamy was when Patrick Sherrill walked into the Edmond post office and killed several of the other employees and then committed suicide. (I only mention this because I worked there at the same time as Patrick Sherrill. I was a distribution clerk and he was a carrier. I took his mail to him after it had been sorted. It is kind of scary to think that my work station -- the PO Boxes from 400-1200 -- was the area where he killed the most people. I guess in hindsight I should count being let go during my probation just prior to this incident as being a blessing in disguise.)

Piedmont, which is northwest of Oklahoma City is a small community where many parents are moving to for its public schools, which are considered to be among the best in the Oklahoma City area.

Mustang is southwest of Oklahoma City and has the same reputation as Piedmont. The home values in Mustang and Piedmont have risen very fast in the last few years. I guess if there are bubble areas of Oklahoma City, this would be two of them.

Houses in the OKC area will generally range from $45 per square foot for less desirable areas to $80 sf for the nicest areas (like the ones I was looking for). For the most part, most of OKC is very affordable and can be bought by middle income earners for 20% down and 20% of gross income -- which is the general rule for home affordability. A check on the Multi Listing System (MLS) will confirm that it is possible to buy medium-sized home with yard space for kids and pets for a reasonable price.

I suspect Oklahoma City and the surrounding area will get hit by the Housing Bubble we hear so much about in a few years, but I somehow doubt that we will get hit as hard.

While life is slower here, we still have access to things that other big cities have; but you will probably encounter fewer stressed-out, rude people in the process of enjoying them.

Tuesday, October 17, 2006

An anonymous comment

Someone who I met online sent me a personal email responding to my request on what they want to hear about.

I personally like your entries on Christian or faith-based issues, medical care and the law. For example, I wanted to know more about the habeas corpus issue -- what exactly does it do for average citzens, what the threat was, etc.

If you want more readers, I would have to say -- focus on housing in Oklahoma. People seem to want to read about housing -- prices, rip-offs, declines, where it's still cheap, etc.

I think what makes any blog compelling is original content. 99% are just links to other content, so what value is being added? Opinion doesn't really get people to come back, either, because its generally uninformed -- except for the super-ideologue sites where people preach to the choir. Not my taste, that's for sure.

Hope this helps...

Thanks for the comment. I will try to implement your suggestions. I was already planning to write another article about Habeas Corpus now that President Bush signed the Military Commissions Act into law today.

I definitely have something to think about from this email, however.

I personally like your entries on Christian or faith-based issues, medical care and the law. For example, I wanted to know more about the habeas corpus issue -- what exactly does it do for average citzens, what the threat was, etc.

If you want more readers, I would have to say -- focus on housing in Oklahoma. People seem to want to read about housing -- prices, rip-offs, declines, where it's still cheap, etc.

I think what makes any blog compelling is original content. 99% are just links to other content, so what value is being added? Opinion doesn't really get people to come back, either, because its generally uninformed -- except for the super-ideologue sites where people preach to the choir. Not my taste, that's for sure.

Hope this helps...

Thanks for the comment. I will try to implement your suggestions. I was already planning to write another article about Habeas Corpus now that President Bush signed the Military Commissions Act into law today.

I definitely have something to think about from this email, however.

David Kuo talks about his new book

Are Christian leaders being naïve in their dealings with the White House or do they understand the nature of the exchange?

It’s a little bit of both. In some ways White House power is like [J.R.R.] Tolkien’s ring of power. When you put it on, it feels good and it’s dazzling. But after a while it begins to consume you in ways you don’t realize. That’s the nature of White House power. I have no doubt that Christian political leaders have gotten involved for all the right reasons. I just think over time it becomes harder and harder to stand up against that ring of power and the White House, to say no and walk away.

The Christian political leaders have been seduced. If you look at their comments that they know what they’re doing, I’m not quite sure how to read that—is it wonderful or a little troubling? That’s one of the reasons I call for this fast from politics.

Amen to that.

It’s a little bit of both. In some ways White House power is like [J.R.R.] Tolkien’s ring of power. When you put it on, it feels good and it’s dazzling. But after a while it begins to consume you in ways you don’t realize. That’s the nature of White House power. I have no doubt that Christian political leaders have gotten involved for all the right reasons. I just think over time it becomes harder and harder to stand up against that ring of power and the White House, to say no and walk away.

The Christian political leaders have been seduced. If you look at their comments that they know what they’re doing, I’m not quite sure how to read that—is it wonderful or a little troubling? That’s one of the reasons I call for this fast from politics.

Amen to that.

Monday, October 16, 2006

USA Today article about American Health Care

From the article:

So what's driving the rapid rise of health care spending ?

Major drivers of medical inflation include how rapidly Americans embrace new drugs and technology, which are often more expensive than older treatments. Public demand is a big factor. Patients generally want the newest treatment, equating new with "better," even before solid proof exists.

Other factors include rising prices for medical services, particularly hospital prices, growing labor costs and waste and inefficiency. America's obesity epidemic is also fueling spending on medical care.

Americans did not always select the same culprits for rising spending as do economists.

In the survey, only 28% picked new drugs, treatments and technology as among the single biggest factors, while the smallest percentage, 12%, said costs are rising because more people are getting better medical care than ever before.

Half of respondents blamed profits of drug and insurance companies as one of the single biggest factors, while 37% blamed too many medical malpractice lawsuits, and 36% blamed doctors and hospitals making too much money.

"Profits might explain part of why costs are high, but it doesn't explain why costs are rising," says Paul Ginsburg, an economist at the Center for Studying Health System Change. New treatments and increased demand are fueling the rise, he says.

"The thing I find dismaying is the public doesn't recognize that it's the additional medical care they're getting that's driving costs up," Ginsburg says. "They have to come to grips with the fact that we won't be able to slow the rise in costs without making trade-offs."

...

Poll respondents were closer when it came to fraud and waste, with 37% choosing it as one of the biggest drivers. Reinhardt and others have said that fraud along with overuse and waste are big players in rising costs. Overuse and waste can include unnecessary treatments, tests repeated because original results were misplaced or reliance on ineffective treatments.

"Several credible estimates have come up with around 30% of health care is unnecessary," says Richard Deyo, professor of medicine at the University of Washington in Seattle. "I suspect even an ideal system would have some unnecessary care delivered, but 30% seems a high percentage."

Few saw any consumer responsibility in rising costs, with only 29% citing Americans' unhealthy lifestyles as one of the biggest factors.

___________________

The USA Today feature also included an article that gave consideration to Universal Health Care. The article can be found here.

In the article, the poll sponsored by USA Today, ABC News and the Kaiser Family Foundation found that a majority of Americans (56%) favor creating universal coverage for every American. Sixty-eight percent of Americans believe creating a universal health care system is more important than keeping taxes down. So much for the Republican argument that people always hate tax increases.

We can create a universal system that saves costs and saves lives. The poll shows that a majority of Americans support creating a universal system. Universal health care is an idea whose time has come. All we need to do now is vote for candidates who will go on the record supporting it.

So what's driving the rapid rise of health care spending ?

Major drivers of medical inflation include how rapidly Americans embrace new drugs and technology, which are often more expensive than older treatments. Public demand is a big factor. Patients generally want the newest treatment, equating new with "better," even before solid proof exists.

Other factors include rising prices for medical services, particularly hospital prices, growing labor costs and waste and inefficiency. America's obesity epidemic is also fueling spending on medical care.

Americans did not always select the same culprits for rising spending as do economists.

In the survey, only 28% picked new drugs, treatments and technology as among the single biggest factors, while the smallest percentage, 12%, said costs are rising because more people are getting better medical care than ever before.

Half of respondents blamed profits of drug and insurance companies as one of the single biggest factors, while 37% blamed too many medical malpractice lawsuits, and 36% blamed doctors and hospitals making too much money.

"Profits might explain part of why costs are high, but it doesn't explain why costs are rising," says Paul Ginsburg, an economist at the Center for Studying Health System Change. New treatments and increased demand are fueling the rise, he says.

"The thing I find dismaying is the public doesn't recognize that it's the additional medical care they're getting that's driving costs up," Ginsburg says. "They have to come to grips with the fact that we won't be able to slow the rise in costs without making trade-offs."

...

Poll respondents were closer when it came to fraud and waste, with 37% choosing it as one of the biggest drivers. Reinhardt and others have said that fraud along with overuse and waste are big players in rising costs. Overuse and waste can include unnecessary treatments, tests repeated because original results were misplaced or reliance on ineffective treatments.

"Several credible estimates have come up with around 30% of health care is unnecessary," says Richard Deyo, professor of medicine at the University of Washington in Seattle. "I suspect even an ideal system would have some unnecessary care delivered, but 30% seems a high percentage."

Few saw any consumer responsibility in rising costs, with only 29% citing Americans' unhealthy lifestyles as one of the biggest factors.

___________________

The USA Today feature also included an article that gave consideration to Universal Health Care. The article can be found here.

In the article, the poll sponsored by USA Today, ABC News and the Kaiser Family Foundation found that a majority of Americans (56%) favor creating universal coverage for every American. Sixty-eight percent of Americans believe creating a universal health care system is more important than keeping taxes down. So much for the Republican argument that people always hate tax increases.

We can create a universal system that saves costs and saves lives. The poll shows that a majority of Americans support creating a universal system. Universal health care is an idea whose time has come. All we need to do now is vote for candidates who will go on the record supporting it.

9 Simple Points of Investing for Ordinary People

From the Big Picture Blog (see link in sidebar).

1. Make a will

2 .Pay off your credit cards

3. Get term life insurance if you have a family to support

4. Fund your 401k to the maximum

5. Fund your IRA to the maximum

6. Buy a house if you want to live in a house and can afford it

7. Put six months worth of expenses in a money-market account

8. Take whatever money is left over and invest 70% in a stock index fund and 30% in a bond fund through any discount broker and never touch it until retirement

9. If any of this confuses you, or you have something special going on (retirement, college planning, tax issues), hire a fee-based financial planner, not one who charges a percentage of your portfolio

1. Make a will

2 .Pay off your credit cards

3. Get term life insurance if you have a family to support

4. Fund your 401k to the maximum

5. Fund your IRA to the maximum

6. Buy a house if you want to live in a house and can afford it

7. Put six months worth of expenses in a money-market account

8. Take whatever money is left over and invest 70% in a stock index fund and 30% in a bond fund through any discount broker and never touch it until retirement

9. If any of this confuses you, or you have something special going on (retirement, college planning, tax issues), hire a fee-based financial planner, not one who charges a percentage of your portfolio

Saturday, October 14, 2006

What do my readers want to hear about?

I have been trying to find some niche in the blogger market that needs to be filled. Charles Smith of the Of Two Minds referred to me as a "polymath" in an email to me. (I had to look up the word. It means a person of great learning or "Renaissance Man." As in, see Leonardo Da Vinci.) It was quite a compliment, but I am probably more of a "jack of all trades and master of none" than a true expert in any given field. Except for the game of chess, of course -- where I really did become a National Master by USCF standards. But if I wanted to try to do a regular column about chess, I would create another blog (not that I won't at some point in the future).

So my question to you, my 24 regular readers (Karl, Teri, Charles and anyone else reading) what answers to life's great questions do you want answered? What news stories are you most following? What would you like me to write about?

So my question to you, my 24 regular readers (Karl, Teri, Charles and anyone else reading) what answers to life's great questions do you want answered? What news stories are you most following? What would you like me to write about?

How do bankers make money on subprime?

The poster "Tanta" over at the Calculated Risk blog (see sidebar for link) gives an explanation on how mortgage lenders make on subprime loans:

1. Charge big upfront origination fees.

2. Charge big late fees. The most profitable subprime borrower is the one who is always 30 days behind (the "rolling 30").

3. Put borrowers into subprime even though they could qualify for prime credit. (This is called "predatory lending.")

4. Charge very high interest rates.

5. Keep your maximum LTV at 80% or less. That way, you will at least break even on a foreclosure.

It should be said that Tanta is considered to be a resident expert over at one of the most respected (and visited) macroeconomic blogs out there. The problem with contemporary loans, she says, is that the lenders have forgotten about Rule #5.

***Update***

A poster at Calculated Risk's blog asked how lenders "expect to make money on high foreclosure loans. "

Poster "mort_fin" posted a response (I have edited it for grammar and clarity):

"The math is as follows:

Charge 2 points upfront, then charge a 300 bp spread. Insist on a 5 year prepayment penalty. How much foreclosure will that cover?

Assume that you lose 40% for each loan that goes bad (that's worse than average, which is in the 30's).

Assume that loans that go bad do so, on average, 2 years after origination.

You've made 800 bp in the first 2 years (200 upfront, and 300 a year for 2 years). If 30% of the loans go bad, you make (300 a year for 3 years on 1/2) another 450. That totals 1250 basis points. Foreclosures cost you 30% (loans gone bad) x 40% (loss per loan) or 1200 basis points. With a 30% foreclosure rate you're 50 bp ahead - plus a few of those loans will continue to pay the high spread after year 5 - pure gravy. You can have pretty stiff foreclosure rates and still make a buck -- especially if you can keep your loss per loan down around 30% instead of up around 40%."

In other words, why should lenders care about the customer/consumer if they make money even on bad loans? The whole system sounds predatory to me.

1. Charge big upfront origination fees.

2. Charge big late fees. The most profitable subprime borrower is the one who is always 30 days behind (the "rolling 30").

3. Put borrowers into subprime even though they could qualify for prime credit. (This is called "predatory lending.")

4. Charge very high interest rates.

5. Keep your maximum LTV at 80% or less. That way, you will at least break even on a foreclosure.

It should be said that Tanta is considered to be a resident expert over at one of the most respected (and visited) macroeconomic blogs out there. The problem with contemporary loans, she says, is that the lenders have forgotten about Rule #5.

***Update***

A poster at Calculated Risk's blog asked how lenders "expect to make money on high foreclosure loans. "

Poster "mort_fin" posted a response (I have edited it for grammar and clarity):

"The math is as follows:

Charge 2 points upfront, then charge a 300 bp spread. Insist on a 5 year prepayment penalty. How much foreclosure will that cover?

Assume that you lose 40% for each loan that goes bad (that's worse than average, which is in the 30's).

Assume that loans that go bad do so, on average, 2 years after origination.

You've made 800 bp in the first 2 years (200 upfront, and 300 a year for 2 years). If 30% of the loans go bad, you make (300 a year for 3 years on 1/2) another 450. That totals 1250 basis points. Foreclosures cost you 30% (loans gone bad) x 40% (loss per loan) or 1200 basis points. With a 30% foreclosure rate you're 50 bp ahead - plus a few of those loans will continue to pay the high spread after year 5 - pure gravy. You can have pretty stiff foreclosure rates and still make a buck -- especially if you can keep your loss per loan down around 30% instead of up around 40%."

In other words, why should lenders care about the customer/consumer if they make money even on bad loans? The whole system sounds predatory to me.

Are Democrats winning due to good looks?

The idea that better looking people are more successful is not new. The theory is called "Lookism." See this news story done by ABC's John Stossel a while back.

I think the idea definitely has merit. While I was in law school, they showed us a film where they did a story on a fictional trial using high-school students. The jury pools, however, did not know that it was fake. The study kept things as close to the same for both trials as possible. They used the same description of the defendants, the same attorneys, the same arguments for both sides, the same rulings on the objections and so on.

For the Defendants, they used an "ordinary" looking defendant and a football quarterback who had been picked Prom King of his school. Guess what the result of the trials was? The ordinary-looking boy was convicted, while the football quarterback was acquitted.

As to the story in the Washington Post: generally speaking, both political parties usually nominate the better looking candidate. Although I wouldn't totally discount the story, I don't think that it's the best explanation for what is happening this time around.

I think the idea definitely has merit. While I was in law school, they showed us a film where they did a story on a fictional trial using high-school students. The jury pools, however, did not know that it was fake. The study kept things as close to the same for both trials as possible. They used the same description of the defendants, the same attorneys, the same arguments for both sides, the same rulings on the objections and so on.

For the Defendants, they used an "ordinary" looking defendant and a football quarterback who had been picked Prom King of his school. Guess what the result of the trials was? The ordinary-looking boy was convicted, while the football quarterback was acquitted.

As to the story in the Washington Post: generally speaking, both political parties usually nominate the better looking candidate. Although I wouldn't totally discount the story, I don't think that it's the best explanation for what is happening this time around.

Friday, October 13, 2006

Household Debt Service Ratio continues to increase

For some good analysis and a graph comparing mortgage ratios and DSR click on the Calculated Risk link in the sidebar.

One thing I am sure of, even though I am not smart enough to provide technical analysis of the numbers, I know they are not good. If you look at the ratios starting from 80q1 (1st Quarter of 1980) to 06q2 (2nd Quarter of 2006) they steadily increase. I take this to mean that American households are servicing more debt than ever. Soon we will reach a breaking point where there will be too much debt to provide economic recovery stimulus.

Combine this with ever-expanding government debt and deficits as far as the eye can see, and you have the potential for the makings of a economic perfect storm.

Will we ever be able to start paying down our collective debt?

It wasn't too long ago that Alan Greenspan complained about "excess liquidity" (as in, too much savings and not enough borrowing) in the Asian markets. The problem is not too much liquidity in their markets, the problem is not enough savings in ours. When consumers making $40-50K per year are encouraged to buy a house for $500K and add other consumer debt on top of that.

Something has got to give. The continually increasing debt burden on both a personal and governmental level will limit our ability to grow the economy during times of economic contraction. The answer at this point is to start paying down both personal and governmental debt -- the sooner the better.

One thing I am sure of, even though I am not smart enough to provide technical analysis of the numbers, I know they are not good. If you look at the ratios starting from 80q1 (1st Quarter of 1980) to 06q2 (2nd Quarter of 2006) they steadily increase. I take this to mean that American households are servicing more debt than ever. Soon we will reach a breaking point where there will be too much debt to provide economic recovery stimulus.

Combine this with ever-expanding government debt and deficits as far as the eye can see, and you have the potential for the makings of a economic perfect storm.

Will we ever be able to start paying down our collective debt?

It wasn't too long ago that Alan Greenspan complained about "excess liquidity" (as in, too much savings and not enough borrowing) in the Asian markets. The problem is not too much liquidity in their markets, the problem is not enough savings in ours. When consumers making $40-50K per year are encouraged to buy a house for $500K and add other consumer debt on top of that.

Something has got to give. The continually increasing debt burden on both a personal and governmental level will limit our ability to grow the economy during times of economic contraction. The answer at this point is to start paying down both personal and governmental debt -- the sooner the better.

Jury Finds Wal-Mart Guilty of Labor Law Violations

PHILADELPHIA - A state jury found Thursday that Wal-Mart broke Pennsylvania labor laws by forcing employees to work through rest breaks and off the clock, a decision plaintiffs' lawyers said would result in at least $62 million in damages.

The Bentonville, Ark.-based retail giant is facing a slew of similar suits around the country.

***Update***

Jury awards $78 million in damages in Wal-Mart labor violations case.

A similar lawsuit to this is being litigated here in Oklahoma. Considering the commonality of the type of violations being reported in the Pennsylvania case referenced in the header link, I feel pretty confident that it was the result of a policy of Wal-Mart's owners and upper management.

They will continue to deny it, and will probably appeal the final verdict, but I think this is just more evidence the zeitgeist of the country right now. There is just a type of malaise that has set out on the public. Enron, WorldCom and others essentially stealing worker's pensions and dumping obligations to pay for health care right when those workers need it most in Chapter 11 bankruptcies. This case of Wal-Mart abusing its workers. CEOs and upper management giving themselves lavish compensation awards while telling the workers that there is not enough available to fund their pensions. Their enablers in Congress who are being proven to be utterly corrupt. And the hypocrisy of the Republican party promising conservative Christians that they would cater to their desires -- only to have been exposed as cynically using them so that they could carry out the above abuses is apparently going to revealed in a soon-to-be-released book Tempting Faith: An Inside Story of Political Seduction by David Kuo .

After only two years of the Republicans controlling both houses of Congress and the White House, the tide of history seems to have changed. With gerrymandered congressional districts that seemed to have etched the Republican majority in stone and with more voting power having moved to give Republican strongholds of rural and religous voters more power, such a sea change would have been unthinkable even earlier this year. All of a sudden it seems like even the most fervent Republican base voters are coming to the realization that they have been had. Many of them are coming to the realization that they have been played for suckers. The conservative Christians are starting to realize the wisdom of Jesus saying "you cannot serve God and money."

No amount of change from the election will be enough. So much damage has been done already that I find it hard to believe that we can get a "reversion to the mean" in terms of Justice. But, at least it would be a start.

The Bentonville, Ark.-based retail giant is facing a slew of similar suits around the country.

***Update***

Jury awards $78 million in damages in Wal-Mart labor violations case.

A similar lawsuit to this is being litigated here in Oklahoma. Considering the commonality of the type of violations being reported in the Pennsylvania case referenced in the header link, I feel pretty confident that it was the result of a policy of Wal-Mart's owners and upper management.

They will continue to deny it, and will probably appeal the final verdict, but I think this is just more evidence the zeitgeist of the country right now. There is just a type of malaise that has set out on the public. Enron, WorldCom and others essentially stealing worker's pensions and dumping obligations to pay for health care right when those workers need it most in Chapter 11 bankruptcies. This case of Wal-Mart abusing its workers. CEOs and upper management giving themselves lavish compensation awards while telling the workers that there is not enough available to fund their pensions. Their enablers in Congress who are being proven to be utterly corrupt. And the hypocrisy of the Republican party promising conservative Christians that they would cater to their desires -- only to have been exposed as cynically using them so that they could carry out the above abuses is apparently going to revealed in a soon-to-be-released book Tempting Faith: An Inside Story of Political Seduction by David Kuo .

After only two years of the Republicans controlling both houses of Congress and the White House, the tide of history seems to have changed. With gerrymandered congressional districts that seemed to have etched the Republican majority in stone and with more voting power having moved to give Republican strongholds of rural and religous voters more power, such a sea change would have been unthinkable even earlier this year. All of a sudden it seems like even the most fervent Republican base voters are coming to the realization that they have been had. Many of them are coming to the realization that they have been played for suckers. The conservative Christians are starting to realize the wisdom of Jesus saying "you cannot serve God and money."

No amount of change from the election will be enough. So much damage has been done already that I find it hard to believe that we can get a "reversion to the mean" in terms of Justice. But, at least it would be a start.

Thursday, October 12, 2006

Nice Rent vs. Purchase home spreadsheet

This is a nice little spreadsheet that Google has made available to help you determine if purchasing a home or renting is the better economic decision.

Free registration required.

Free registration required.

Wednesday, October 11, 2006

The Problem with Panhandlers

One of the problems with panhandlers is that vast majority of them do not need financial help. Another problem is that they lead us to become cynical. People who truly need help have a harder time getting it. We don't know if they are honest, or if they are just trying to con us for drug money.

Believe it or not, there are actually schools where people learn how to panhandle -- and the good ones can make more money panhandling than actually working at something productive. Such activity should be discouraged. Everyone should contribute what they can. I also think that Social Security disability should be changed to provide for temporary and partial disability claims. The current system is based on an all-or-nothing basis. It is both overinclusive and underinclusive in its scope. But that's a story for some future blog.

Panhandlers also make patrons of businesses avoid the area, which lead to less money available. The National Coalition for the Homeless doesn't like anti-panhandling ordinances, but I for one don't like having to deal with agressive panhandlers. Many of them have drug or alcohol problems and they sometimes will act unpredictably. I have no problem supporting tax dollars to be used to treat their illnesses, to provide them with a place to sleep or any other temporary assistance to help them get on their feet, but I don't want them in my face making me feel unsafe on the street.

One of the downsides to the revitalization of Bricktown in downtown Oklahoma City has been the appearance of panhandlers in the parking lots and along the canal. Sometimes they will try to pose as parking attendants and collect parking fees after the parking lots have closed.

There has to be some way to deal with such a problem while still helping the truly needy.

Believe it or not, there are actually schools where people learn how to panhandle -- and the good ones can make more money panhandling than actually working at something productive. Such activity should be discouraged. Everyone should contribute what they can. I also think that Social Security disability should be changed to provide for temporary and partial disability claims. The current system is based on an all-or-nothing basis. It is both overinclusive and underinclusive in its scope. But that's a story for some future blog.

Panhandlers also make patrons of businesses avoid the area, which lead to less money available. The National Coalition for the Homeless doesn't like anti-panhandling ordinances, but I for one don't like having to deal with agressive panhandlers. Many of them have drug or alcohol problems and they sometimes will act unpredictably. I have no problem supporting tax dollars to be used to treat their illnesses, to provide them with a place to sleep or any other temporary assistance to help them get on their feet, but I don't want them in my face making me feel unsafe on the street.

One of the downsides to the revitalization of Bricktown in downtown Oklahoma City has been the appearance of panhandlers in the parking lots and along the canal. Sometimes they will try to pose as parking attendants and collect parking fees after the parking lots have closed.

There has to be some way to deal with such a problem while still helping the truly needy.

The End of Habeas Corpus?

***Updated link above***

It's not up yet, but Keith Olbermann had a segment on Tuesday night's show (October 10, 2006) regarding the Bush Administration and the Republicans in Congress seeking to abolish the Writ of Habeas Corpus. This ought to shock every American. The Great Writ, as it is called in legal circles, is the foundation upon which freedom in America is based.

Article 1, Section 9, Clause 2 of the U.S. Constitution:

The privilege of the writ of habeas corpus shall not be suspended, unless when in cases of rebellion or invasion the public safety may require it.

There is no rebellion here in America (yet). There is no foreign invasion, either. As for Al Qaeda, they are just ordinary criminals whose motive is to create some fantasy "caliphate."

If Congress abolishes the Writ of Habeas Corpus, we won't be on a "slippery slide toward dictatorship" as former Supreme Court Justice Sandra Day O'Connor called it. We will be there already.

The mere fact the Republicans are seriously talking about this ought to be enough to severely punish them at the polls in November. If we get there in time.

It's not up yet, but Keith Olbermann had a segment on Tuesday night's show (October 10, 2006) regarding the Bush Administration and the Republicans in Congress seeking to abolish the Writ of Habeas Corpus. This ought to shock every American. The Great Writ, as it is called in legal circles, is the foundation upon which freedom in America is based.

Article 1, Section 9, Clause 2 of the U.S. Constitution:

The privilege of the writ of habeas corpus shall not be suspended, unless when in cases of rebellion or invasion the public safety may require it.

There is no rebellion here in America (yet). There is no foreign invasion, either. As for Al Qaeda, they are just ordinary criminals whose motive is to create some fantasy "caliphate."